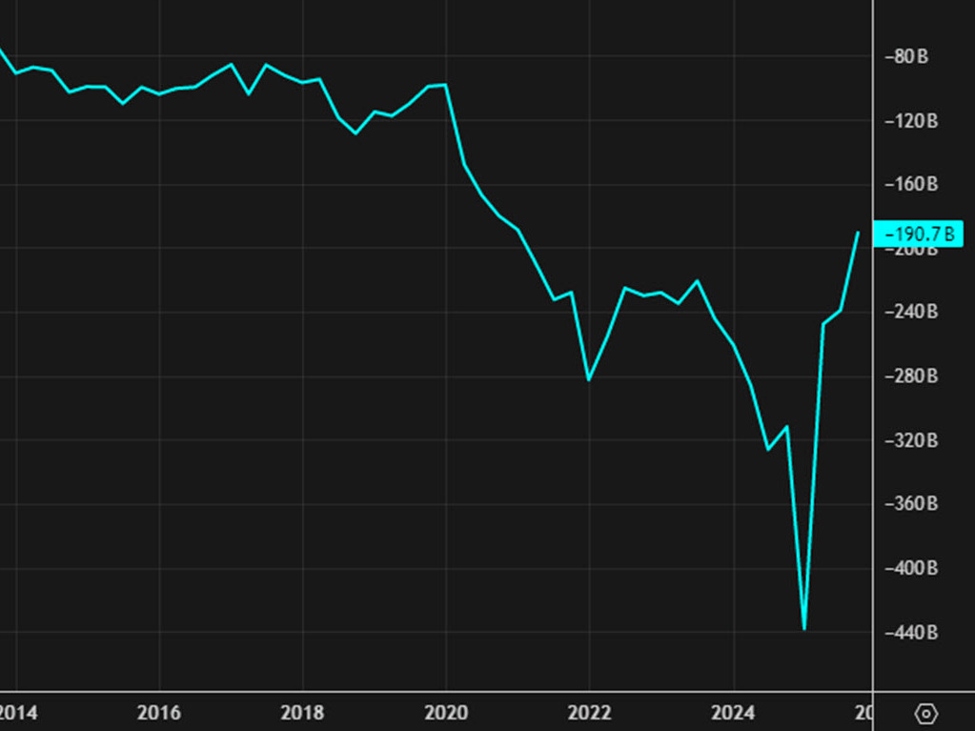

- Prior was -$190.7 billion

The US current account deficit widened to $226.8 billion in Q1, a $5.8 billion or 2.6% deterioration from the revised $221.1 billion in Q4. As a share of GDP it ticked up to 2.9% from 2.8%.

The widening wasn’t about trade. The goods deficit actually narrowed, and exports of goods and services jumped $50.0 billion to $1.38 trillion. The culprit was primary income, which flipped from a Q4 surplus into a Q1 deficit. That’s the income Americans earn on foreign assets versus what foreigners earn here, and the swing tells you something about relative returns and the rising cost of servicing a balance sheet that keeps getting more lopsided.

Imports climbed $55.8 billion to $1.61 trillion, outpacing the export gain. Front-running tariffs or genuine demand? The data won’t settle that argument, but the goods import surge alongside a narrower goods deficit suggests exporters had a decent quarter regardless.

The bigger number sits in the investment position. Net IIP improved to –$21.27 trillion from a revised –$21.87 trillion, but don’t mistake that for deleveraging. It was driven by a $1.18 trillion price decline knocking down the value of US liabilities — foreigners’ US holdings got cheaper, not fewer. Financial transactions still showed $803.7 billion flowing in. The world keeps funding America.

Worth flagging: the annual revisions were heavy. Q4’s deficit was bumped from a preliminary –$190.7 billion to –$221.1 billion, and the net IIP was revised by nearly $6 trillion. Benchmark surveys and new methodology reshaped the picture meaningfully, so anyone anchored to the prior vintage needs to recalibrate.

Net-net: the headline deficit widened, but trade improved and the income drag did the damage. The structural story — a deficit reliant on persistent foreign financing — is unchanged.

Leave a Reply