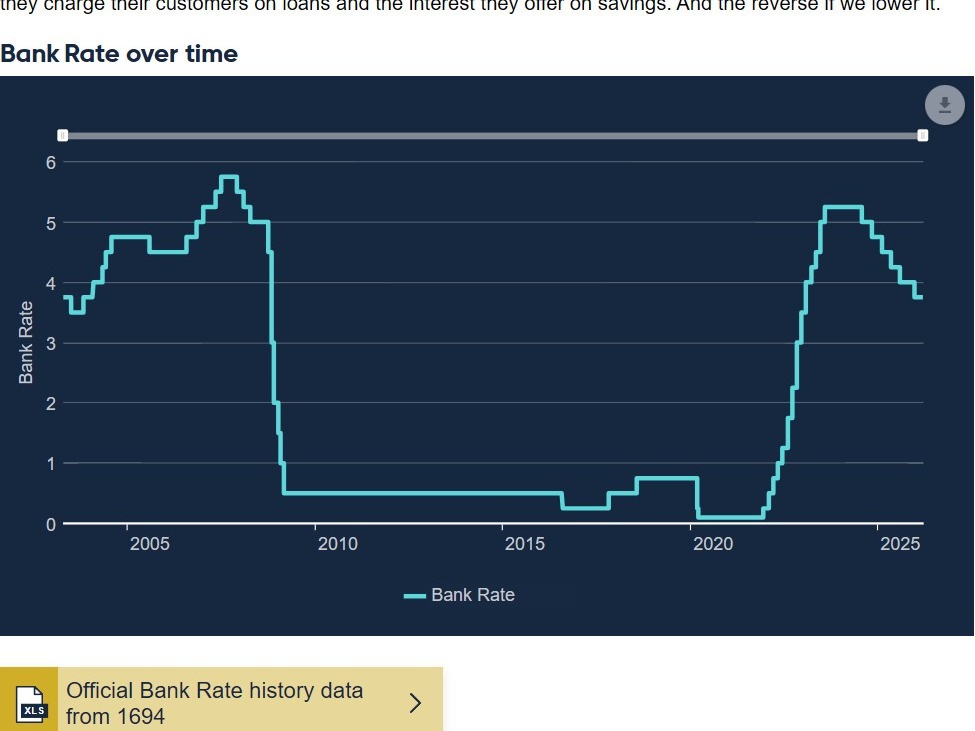

The Bank of England is expected to hold Bank Rate at 3.75% on Thursday in an 8-1 vote, with new forecasts set to show higher inflation and weaker growth as the MPC assesses the Iran war’s economic fallout.

Earlier:

Summary:

- All 62 economists in a Reuters poll predicted the MPC will keep Bank Rate at 3.75%, with most expecting an 8-1 vote and Chief Economist Huw Pill the most likely dissenter in favour of an immediate hike

- The March meeting produced a unanimous 9-0 hold; any move toward dissent this week would signal a shift in the committee’s internal balance toward tightening

- Governor Andrew Bailey has publicly pushed back against market pricing of rate hikes in 2026, calling such bets premature given uncertainty over the war’s duration and economic impact

- Pill has separately warned against a “wait-and-see” approach, arguing the risk of second-round inflationary effects from energy and food prices justifies a more pre-emptive stance

- Thursday’s Monetary Policy Report will be the BoE’s first detailed post-war set of forecasts; economists expect the BoE to raise its inflation projection and cut its growth outlook

- NIESR revised UK growth down to 0.9% this year and 1.0% in 2027, from earlier forecasts of 1.4% and 1.3%, while projecting inflation will not return to the 2% target until 2028

- BNP forecasts two rate hikes in 2026 as UK inflation potentially peaks near 4.5% early next year, up from 3.3% currently

- Britain’s heavy reliance on natural gas, G7-high gilt yields and political uncertainty around Prime Minister Keir Starmer’s government add additional vulnerability to the energy shock

- Bailey and senior BoE officials will hold a press conference at 1130 GMT, thirty minutes after the rates decision, minutes and new forecasts are released

The Bank of England is expected to hold Bank Rate at 3.75% on Thursday, joining the Federal Reserve, which kept rates unchanged on Wednesday, and the European Central Bank, also on hold this week, in a broadly synchronised pause as major central banks assess whether the Iran war’s energy price shock represents a lasting inflationary threat or a growth-killing drag that will eventually do their tightening work for them.

All 62 economists surveyed by Reuters predicted no change, making the decision itself a formality. The substance of Thursday’s meeting lies elsewhere: in the vote split, the new Monetary Policy Report forecasts and Governor Andrew Bailey’s press conference at 1130 GMT.

The vote is the first live question. March’s 9-0 unanimous hold is expected to give way to an 8-1 split, with Chief Economist Huw Pill the most likely dissenter in favour of an immediate hike. Pill has explicitly cautioned against a “wait-and-see” approach, arguing that waiting for second-round effects from energy prices to materialise before acting risks falling behind the curve. Bailey has taken the opposite public position, telling investors that bets on rate hikes this year are premature given the extent of uncertainty around the war’s duration and economic consequences. The gap between those two stances, played out in the vote count, will set the tone for how markets read the BoE’s direction of travel.

The forecasts are the second and arguably more consequential element. Thursday marks the BoE’s first full set of post-war projections, and economists broadly expect a higher inflation path alongside a lower growth forecast, a stagflationary combination that offers the MPC no straightforward policy prescription. The National Institute of Economic and Social Research cut its UK growth forecast to 0.9% this year and 1.0% in 2027 from prior estimates of 1.4% and 1.3% respectively, while projecting inflation will not return to the 2% target until 2028. BNP Paribas takes a more hawkish view on the inflation side, forecasting two rate hikes in 2026 as UK prices potentially peak near 4.5% early next year against a current reading of 3.3%.

Britain enters this meeting with a particular set of vulnerabilities. Its heavy dependence on natural gas makes the energy shock more direct and acute than for continental peers. UK gilt yields are the highest in the G7, raising the cost of government borrowing and compressing fiscal headroom. Data released last week showed input costs for firms rising sharply, with companies lifting their price expectations at a record pace. And political uncertainty around Prime Minister Keir Starmer’s grip on Downing Street has raised broader questions about fiscal credibility at a moment when the public finances can least afford ambiguity. At least one analyst has noted that the degree of rate hike pricing already embedded in financial markets is itself a tightening force, potentially reducing the need for the MPC to act directly, at least in the near term.

—

1100 GMT is 0700 US Eastern time:

—

A hold is unanimous among forecasters and carries no market surprise. The action is in the forecasts and the vote split. An 8-1 decision with Chief Economist Huw Pill dissenting in favour of a hike would signal meaningful internal tension and keep the prospect of tightening alive, while a return to 9-0 would read as a dovish signal that Bailey’s caution is carrying the room. Thursday’s Monetary Policy Report will be the BoE’s first detailed set of projections since the Iran war began, and a higher inflation forecast alongside a growth downgrade is the base case, a stagflationary combination that gives the committee no clean policy answer.

Britain’s particular vulnerability to the energy shock matters here. The country’s heavy reliance on natural gas, the highest gilt yields in the G7, and a politically weakened government raising questions about fiscal credibility all add to the pressure on sterling and UK rates markets. BNP Paribas expects two hikes in 2026 as inflation potentially peaks near 4.5% early next year, against the current 3.3%. But others argue that market pricing of hikes is itself tightening conditions and may do some of the BoE’s work for it, reducing the need for the MPC to actually pull the trigger.

Leave a Reply