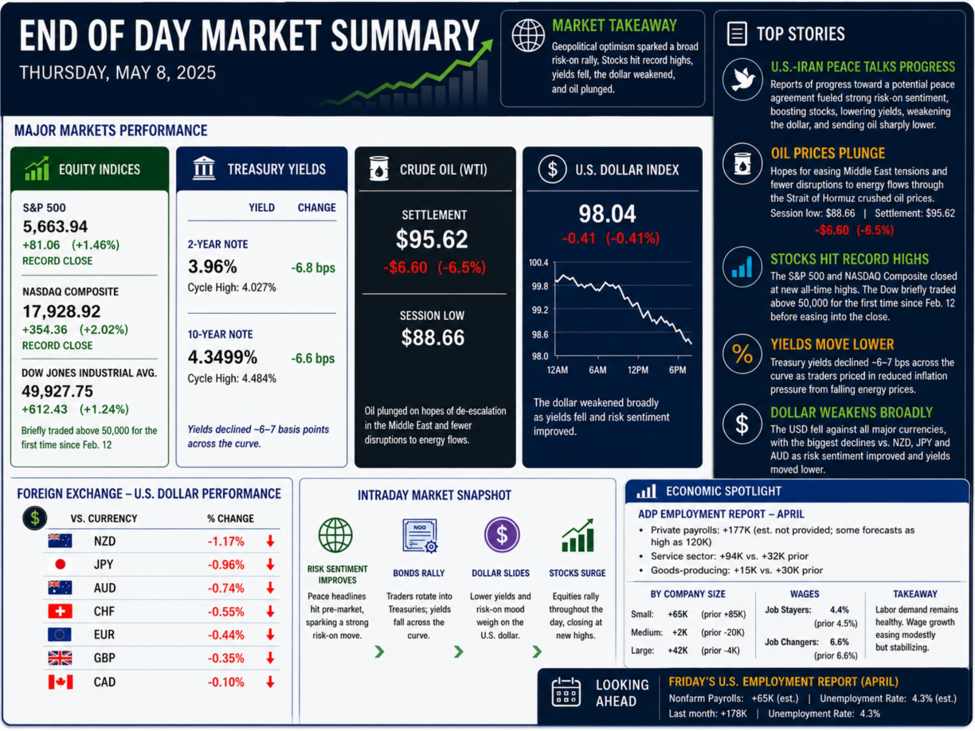

Before North American traders entered for the day, reports surfaced suggesting that the U.S. and Iran were moving closer to a potential peace agreement. The headlines fueled a strong risk-on move across financial markets, sending stocks sharply higher, Treasury yields lower, and the U.S. dollar broadly weaker. Oil prices plunged on hopes that tensions in the Middle East could ease and that disruptions to energy flows through the Strait of Hormuz might eventually subside. Crude oil initially tumbled to a session low of $88.66 before rebounding modestly. Even with the bounce, prices remain sharply lower on the day, with crude currently trading near $95.62, down roughly $6.60 or -6.5%.

The equity market embraced the improving geopolitical backdrop. Both the S&P 500 and the NASDAQ Composite closed at fresh record highs, while the DJIA briefly traded back above the key 50,000 milestone for the first time since February 12 before slipping modestly below that level into the close. Despite the late pullback, the Dow still gained 612 points, or 1.24%, while the NASDAQ surged 2.02% and the S&P advanced 1.46%.

In the U.S. debt market, Treasury yields moved lower across the curve as traders rotated toward safer fixed-income assets and priced in reduced inflation pressure from falling energy prices. Yields declined by roughly 6 to 7 basis points. The 2-year Treasury yield fell 6.8 basis points to 3.96%, while the 10-year yield dropped 6.6 basis points to 4.3499%. For perspective, the recent cycle highs reached 4.027% for the 2-year and 4.484% for the 10-year note.

In the foreign exchange market, the U.S. dollar weakened broadly. The largest declines came against the NZD, JPY, and AUD as improving risk sentiment and lower yields weighed on the greenback. The dollar fell -1.17% versus the NZD, -0.96% against the JPY, and -0.74% versus the AUD. The smallest decline came against the CAD, where the dollar slipped just -0.10%, with falling oil prices helping to offset broader USD weakness.

Aside from the geopolitical headlines, the economic calendar featured the ADP employment report for April. The report pointed to a strengthening U.S. labor market, with private payroll growth accelerating at the fastest pace since January 2025. Service-sector hiring led the gains, adding 94K jobs compared with 32K last month, while goods-producing industries added 15K jobs versus 30K previously. Expectations for a strong report had already been elevated following a series of firm weekly ADP updates, with some forecasts as high as 120K, reinforcing the growing view that the labor market has not only stabilized but may be strengthening again.

By company size, small businesses added 65K jobs, down from 85K previously, while medium-sized firms added just 2K after losing 20K last month. Large companies added 42K jobs following a 4K decline in the prior report, highlighting stronger hiring trends among larger employers. ADP noted that health care, along with a rebound in trade, transportation, and utilities, helped fuel the acceleration in hiring. The agency also pointed out that large companies continue to benefit from greater resources, while smaller firms remain nimble enough to adapt in a more complex labor environment.

On wages, pay growth for workers staying in their jobs eased slightly to 4.4% from 4.5% last month, while wage growth for job changers held steady at 6.6%. The data suggest labor demand remains healthy overall, even as wage pressures show signs of stabilizing rather than reaccelerating.

Looking ahead, attention now turns to Friday’s U.S. employment report. Expectations are for nonfarm payroll growth of 65K following last month’s 178K increase, while the unemployment rate is expected to remain steady at 4.3%.

Leave a Reply