RBI governor Sanjay Malhotra says the rupee may now be undervalued in nominal and real terms after its recent depreciation, and that India’s balance of payments position is not yet a serious concern.

Summary:

Source: RBI Governor Sanjay Malhotra speaking to Mint (gated)

- Malhotra said the rupee is not overvalued and could be considered undervalued in both nominal terms and on a real effective exchange rate basis following its recent slide

- The currency has been approaching the psychologically significant 100-per-dollar mark amid the ongoing West Asia conflict

- The RBI does not target a specific exchange rate level and will only intervene to curb abnormal volatility or undue speculation, Malhotra reiterated

- Despite rising crude prices driven by the conflict, Malhotra described India’s balance of payments position as not yet an undue concern

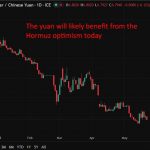

The Indian rupee may have become undervalued following its recent depreciation, Reserve Bank of India Governor Sanjay Malhotra has said, offering a notably relaxed assessment of the currency’s slide as it approaches the psychologically significant level of 100 per dollar.

Speaking to Mint, Malhotra said it would be reasonable to conclude that the rupee is no longer overvalued, and that a case could be made for it having moved into undervalued territory, both in outright nominal terms and when measured against the real effective exchange rate. The REER calculation adjusts for inflation differentials with trading partners and is a closer approximation of whether a currency’s external competitiveness has been eroded or enhanced by its move.

The comments arrive against a backdrop of sustained pressure on the rupee, driven in large part by elevated crude oil prices stemming from the West Asia conflict. India’s dependence on imported energy makes it structurally sensitive to oil price shocks, and a weaker currency amplifies that exposure by raising the local currency cost of each barrel. That combination has focused market attention on whether the RBI would step in to arrest the slide.

Malhotra’s message was that the bar for intervention remains high. The central bank does not target any particular exchange rate level, he said, and would only act to address abnormal volatility or speculative excess rather than to defend a specific floor. That framing gives the RBI operational flexibility while signalling that a move through 100 per dollar would not automatically trigger a defensive response.

On the broader external position, Malhotra sought to anchor expectations. Despite the crude price surge, he described India’s balance of payments situation as not yet an undue concern, a formulation that acknowledges the risk without suggesting it has reached a threshold requiring urgent action.

—

Malhotra’s undervaluation comment is a notable shift in tone that gives the RBI cover to remain on the sidelines rather than defend the rupee aggressively as it approaches the 100-per-dollar level. By framing the currency as cheap on both nominal and real effective exchange rate measures, the governor reduces the political pressure to intervene, while the balance of payments reassurance is aimed at preventing a disorderly sell-off driven by external account fears. Elevated crude prices remain the key vulnerability given India’s import dependence, and any further deterioration in the West Asia conflict could test the RBI’s relaxed framing quickly.

Leave a Reply